When you think about it, Insurance and Risk Management are really the same thing. Adults who own homes have all kinds of insurances including protecting their home and belongings. But when first starting out in the working world, or even before when attending college, insurance is also a big must have – and, like popsicles, Insurance comes in lots of different flavors.

When you think about it, Insurance and Risk Management are really the same thing. Adults who own homes have all kinds of insurances including protecting their home and belongings. But when first starting out in the working world, or even before when attending college, insurance is also a big must have – and, like popsicles, Insurance comes in lots of different flavors.

If you’re renting an apartment, rental insurance is good thing to help protect your belongings in case of a fire, bad weather or even theft. That’s taking your first step with Risk Management. Also health insurance should be on your list. We all know that at age 22, health insurance is the furthest expense to consider. But you should know that a broken arm or a couple of nights at a hospital could put you in serious debt.

So by having insurance that covers your health, your property and even your car is the perfect definition of Risk Management.

April is National Financial Literacy Month, Detective Frank Money’s favorite month! To celebrate the importance of being financially literate, Detective Money is going to post financial literacy tips every day.

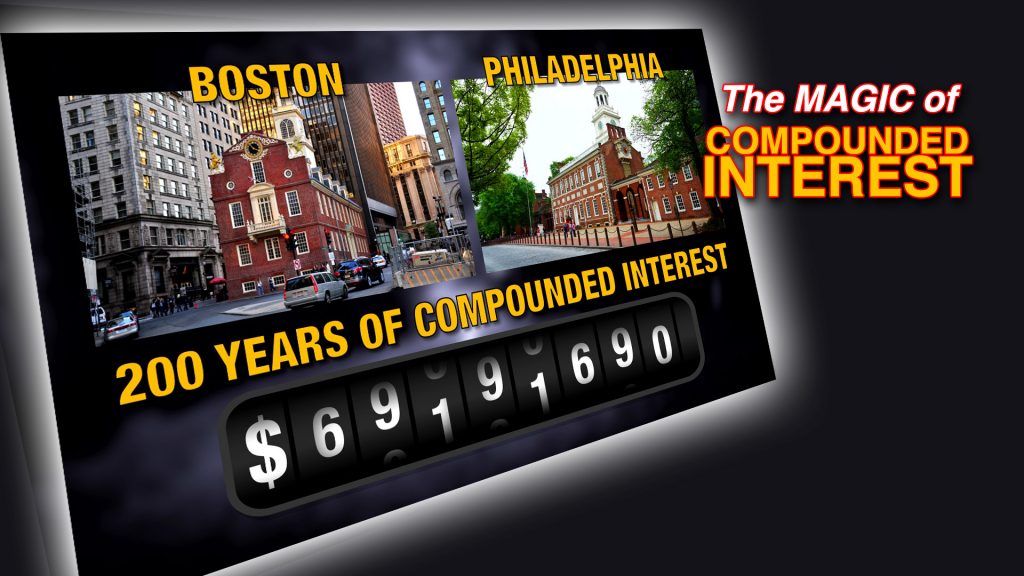

The prettiest two words you ever want to hear when investing are: Compounded Interest. A perfect case comes from the one and only Benjamin Franklin.

The prettiest two words you ever want to hear when investing are: Compounded Interest. A perfect case comes from the one and only Benjamin Franklin. I’m Frank Money, and I wanna help you investigate everything about money! For example, let’s investigate savings. It doesn’t take much detective work to understand that savings is good for you!

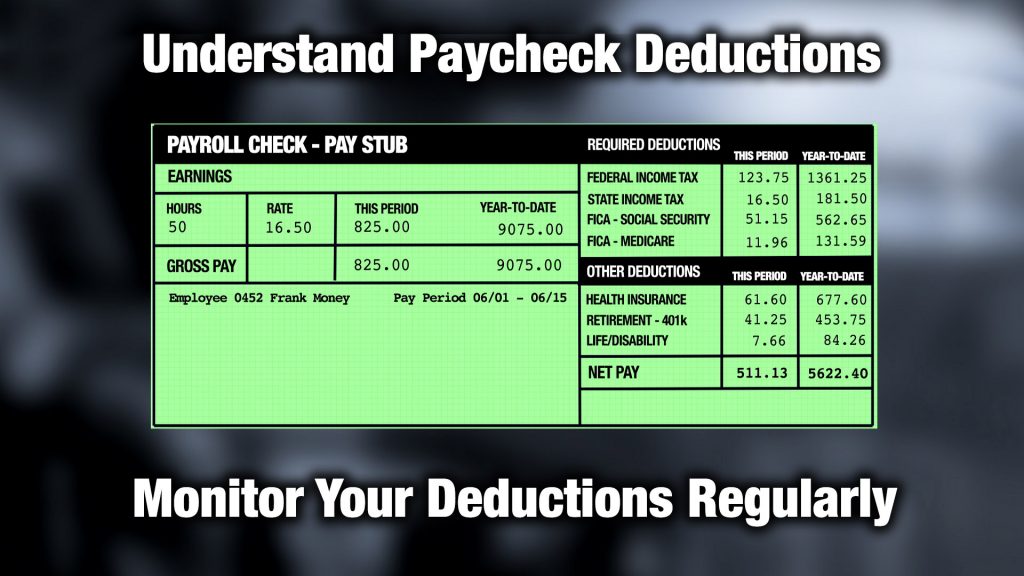

I’m Frank Money, and I wanna help you investigate everything about money! For example, let’s investigate savings. It doesn’t take much detective work to understand that savings is good for you! Getting your first paycheck is an exciting thing. Then you look at the actual amount of the check and you think there must have been a mistake! That’s because they take out taxes and employee benefits from you pay. You should take the time to understand what they deduct from your paycheck, and why.

Getting your first paycheck is an exciting thing. Then you look at the actual amount of the check and you think there must have been a mistake! That’s because they take out taxes and employee benefits from you pay. You should take the time to understand what they deduct from your paycheck, and why.

Student loan debt is a big issue. It is the most common way of funding your college and graduate school education – but doing so has become a ‘Game of Loans’. And since money is my game, you’ll also note it’s my name…. Frank Money that is!…See what I did there?

Student loan debt is a big issue. It is the most common way of funding your college and graduate school education – but doing so has become a ‘Game of Loans’. And since money is my game, you’ll also note it’s my name…. Frank Money that is!…See what I did there? Attention, now, listen up! It’s important to have a personal financial plan. Here is the top ten list for everyone, that will help you with smart money practices and habits:

Attention, now, listen up! It’s important to have a personal financial plan. Here is the top ten list for everyone, that will help you with smart money practices and habits: There’s one private investigator who’s middle name is ‘Identity Theft’! Talkin’ Money’s own Frank Money!

There’s one private investigator who’s middle name is ‘Identity Theft’! Talkin’ Money’s own Frank Money! There’s one private investigator who’s middle name is ‘Organized’! Talkin’ Money’s own Frank Money!

There’s one private investigator who’s middle name is ‘Organized’! Talkin’ Money’s own Frank Money! Identity theft is a serious problem. If someone gains control of your personal information they might be able to open accounts, file taxes and make purchases in your name – and THAT would be a major heist.

Identity theft is a serious problem. If someone gains control of your personal information they might be able to open accounts, file taxes and make purchases in your name – and THAT would be a major heist.