Here’s something I didn’t have to worry about when I went to the school of hard knocks…ROI. That stands for ‘Return On Investment’ when deciding to continue studies with higher education.

The days from the classic film, Animal House, are over. Attending college for 6 years partying. We all know about the spiraling higher education costs per year can go well above $30K! I can safely say graduating with a 4-year college degree in Liberal Arts has gone out with the horse and buggy.

So before going into high debt you should ask yourself what will be my return on the investment I make on my major? How many years will it take to pay back my loans in the field I’ll be working in?

Will the job you get after getting the degree pay off with you making more money over time?You’ve heard the saying ‘Time is Money’? Well in this case it’s ‘Is My Return Be Worth Investing The Extra Money’?

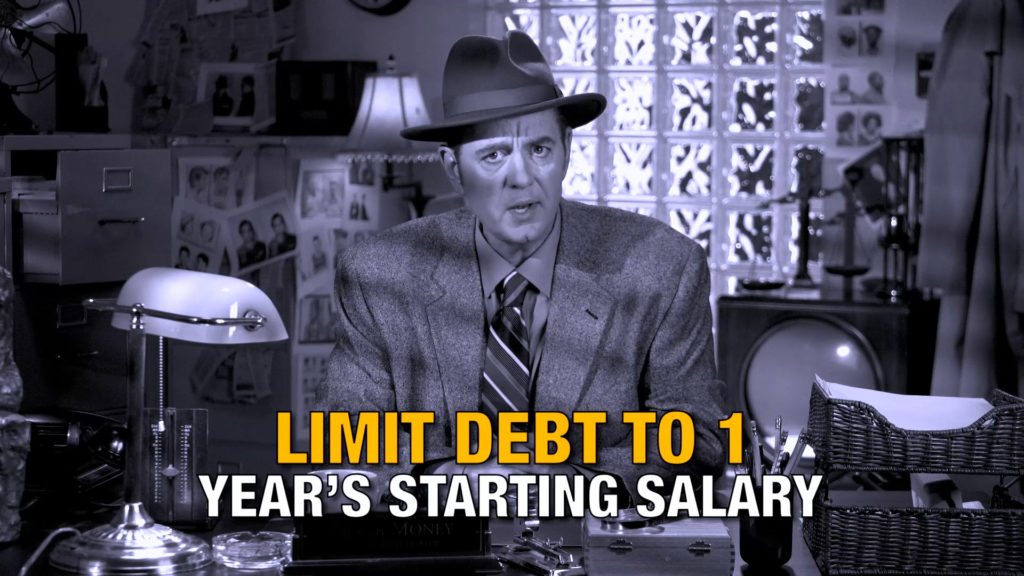

It’s probably a good idea to limit the total amount of debt to one year’s starting salary when it comes to college loans.

It’s okay to pursue your interests but also give yourself a good honest talking to, and a little detective work wouldn’t hurt either, as to whether this investment really going to be worth it for me. Check me out on your local public television station – my show Talkin’ Money Minutes is seen nationwide.

It’s okay to pursue your interests but also give yourself a good honest talking to, and a little detective work wouldn’t hurt either, as to whether this investment really going to be worth it for me. Check me out on your local public television station – my show Talkin’ Money Minutes is seen nationwide.