I’m Frank Money, and I wanna help you investigate everything about money! For example, let’s investigate savings. It doesn’t take much detective work to understand that savings is good for you!

I’m Frank Money, and I wanna help you investigate everything about money! For example, let’s investigate savings. It doesn’t take much detective work to understand that savings is good for you!

And here’s the good news for millennials – you are saving at a rate greater than any generation before you. Fidelity Investments found that 20 somethings are saving on average 7.5% of their income compared to 5.8% in 2013.

We’ve talked about retirement savings, and how important it is to start as soon as you can, along with the benefits of deferring taxes and saving on how much income tax you pay when you invest in a 401k, IRA, etc.

But what about non-retirement savings?

One strategy to employ is to set a goal of savings out of each pay check, and to make that ‘payment’ to you savings account, just like you pay your rent, phone and electric bill. Over time, you grow your savings account and let your money work for you.

What’s the amount you should save? well, it varies from person to person, but a good rule of thumb is to save 10-15% of your gross income (the amount you make BEFORE taxes are deducted) and use that for both your retirement accounts as well as non-retirement accounts.

It takes discipline, but getting used to a regular savings plan is something all millennials need to consider. It doesn’t take much detective work to understand – SAVINGS IS GOOD FOR YOU!

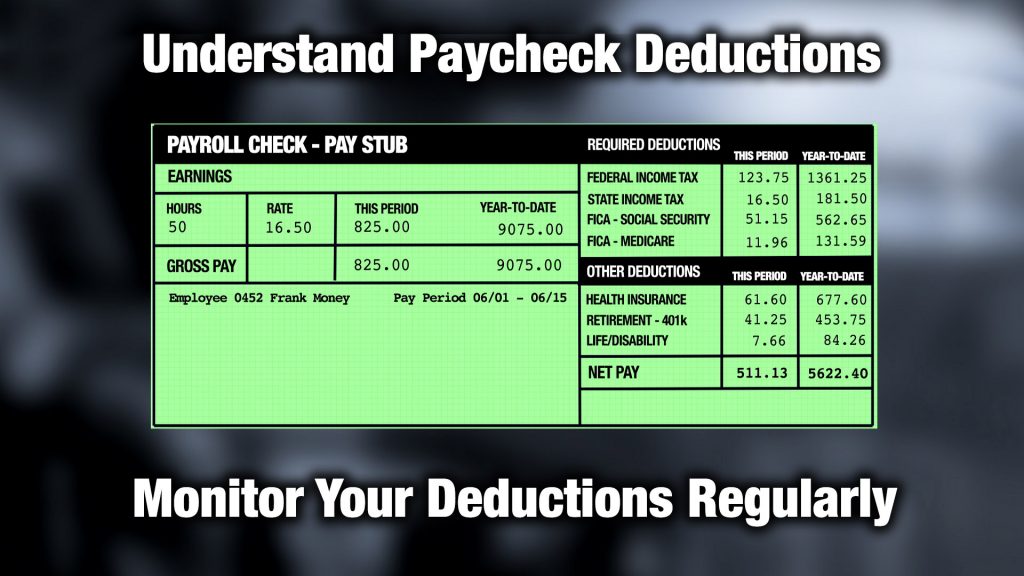

Getting your first paycheck is an exciting thing. Then you look at the actual amount of the check and you think there must have been a mistake! That’s because they take out taxes and employee benefits from you pay. You should take the time to understand what they deduct from your paycheck, and why.

Getting your first paycheck is an exciting thing. Then you look at the actual amount of the check and you think there must have been a mistake! That’s because they take out taxes and employee benefits from you pay. You should take the time to understand what they deduct from your paycheck, and why.