Thanksgiving is the time to be thankful for what you have. But let’s not forget those in need, because charity is also an important part of being financially literate too!

Thanksgiving is the time to be thankful for what you have. But let’s not forget those in need, because charity is also an important part of being financially literate too!

I’m Frank Money – Your very effective money detective.

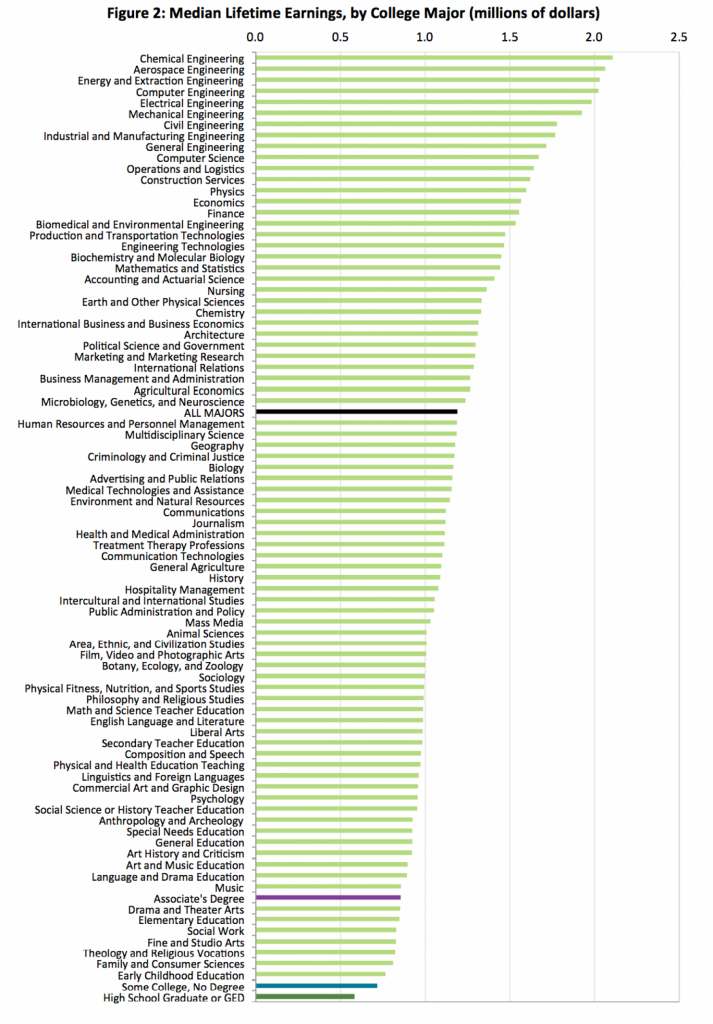

Did you know that YOU are a MILLIONAIRE!

No really, you are. And so is most everyone you know?

How you ask? Well I’ve cracked this case wide open and this Talkin’ Money video explains it!

Through your lifetime, you will most likely earn a million dollars, and probably much more! Here’s a chart showing the Median Lifetime Earnings by College Majors. Just look at the return of a high school degree, versus an Associate’s College Degree and All Majors – it’s pretty amazing!

There was more to the caper than I bargained for – How are you gonna manage your money? It takes responsibility, and, being financially literate!

OK, you need to get around. You need some wheels. But you don’t have a lot of Simoleons…er, Bucks…

OK, you need to get around. You need some wheels. But you don’t have a lot of Simoleons…er, Bucks…

A car is in order right? Well ask yourself – What is the real cost of owning an automobile?

I’m Frank Money, and I want to help you investigate everything about money – This Talkin’ Money video tells the story of one car owner who realized after the fact how much a car really costs.

April is National Financial Literacy Month, Detective Frank Money’s favorite month! To celebrate the importance of being financially literate, Detective Money is going to post financial literacy tips every day.

Frank Money here – your very effective money detective….

Frank Money here – your very effective money detective….

If you have excessive debt, you should take a deep breath and realize you do have options.

Millennials in general have the lowest credit score and most problems managing their debt, compared to prior generations. But the good news is you have the lowest number of credit cards and lowest debt total compared to other generations.

However, the bad news is that you use credit cards a lot, and make a lot of late payments. Late payments mean lower credit scores.

Additionally, millennials tend to use costly alternative financial services, such as auto title loans, payday loans, pawnshops, rent-to-own loans and tax-refund advances.

Here are some steps you can do to help you get control of excessive debt:

1 – For credit cards, get a lower credit card interest rate as soon as you can – Call up your credit card company and ask for a lower rate.

2 – If you can’t make the minimum payments on time, call your credit card company and work out a payment plan.

3 – Allocate a larger portion of your income to reduce debt. This will be painful, but over time it will work.

4 – Limit your spending. If you don;t have a budget plan in place, now is the time. Limit your spending to only the essentials, and make paying off your debt the number one priority.

5 – Motivate yourself. Reach out to friends or relatives who have been through similar problems. This is a process, and it helps to have support during those low times.

Need more help? Then why not reach out to the NFCC (National Foundation for Credit Counseling – the nations largest and longest-serving non-profit financial counseling organization.

So don’t fret the debt – instead take some steps to help yourself and sleep easier.

You really should apply good consumer skills to your purchase decisions. How so you say?

You really should apply good consumer skills to your purchase decisions. How so you say?

Just like my bloodhound ‘Shamus’ would do, it really just takes an analytical, systematic approach to decision making. In fact, you can apply this to lots of things in life.

Well think about it, do you really want to go through life spending more than you have to for things you buy? Or what about paying higher fees for things people get for a lot less, or even for free?

Here’s a step-by-step approach that really helps:

1 – Consider the item, thing or service you want.

2 – Look at several options for each – Let’s say three different ones.

3 – Consider to alternatives and consequences of each option.

4 – Make your decision…go ahead, pick one!

5 – Analyze the results of your choice. Did it turn out the way you wanted? What could your of done differently for a better result?

Congratulations! Now that’s applying good consumer skills. It applies to buying a car, renting a house, purchasing a smart phone, even buying an ice cream cone! In the end, if you think carefully about each purchase, you could save yourself big bucks!

We’ve all heard and read a thousand times how we should save on a regular basis and the younger you start the more we’ll have when getting closer to retirement. But as sure as the sun rises there will always be something that happens in your life that will make it difficult for you to part with your money to put into savings. That’s why every paycheck you should have a set portion of your salary automatically deposited into your savings account.

We’ve all heard and read a thousand times how we should save on a regular basis and the younger you start the more we’ll have when getting closer to retirement. But as sure as the sun rises there will always be something that happens in your life that will make it difficult for you to part with your money to put into savings. That’s why every paycheck you should have a set portion of your salary automatically deposited into your savings account.

I’ve done the detective work on this and the later you wait to start saving, even a year or two, could mean the difference of up to $200,000 or more! Remember compounding interest? Over time your money will make more money for you. Mind blown!

In fact, if you want to have what we financial literacy fans call ‘fun’ here’s a link to the government’s Securities and Exchange Commission’s handy, dandy Compounded Interest Calculator. GO ahead, plug some numbers in, step back, and get ready to be surprised!

https://www.investor.gov/tools/calculators/compound-interest-calculator

Good old Benjamin Franklin once said: “An investment in knowledge pays the best interest.” So it’s up to you to be a wise investor with your savings.

Today’s secret word – Fiduciary!

Today’s secret word – Fiduciary!

Now as words go, this detective finds that word to be a long…and maybe a little intimidating.

But when it comes to your finances, fiduciary is your friend! The definition of the word is “involving TRUST, especially to the relationship of a trustee and a beneficiary.”

In my line of work, trust is a big deal! In the world of money and financing, it establishes how the relationship between you and a financial advisor or institution works.

Here’s a case – Mark wanted to put the money he is saving in his IRA for retirement in a mutual fund. He asked a financial advisor for advice on which fund to purchase. The advisor gave him a couple of choices, but when Mark investigated the funds closer, he discovered that the funds carried high fees. Which would mean, he might make less on his investment over time.

Now there was nothing wrong with the funds the financial advisor recommended, but most likely the reason he recommended them was because the advisor would profit from the sale of the mutual fund to Mark – probably in the form of a commission. Which means that the advisor has some ‘skin in the game’ when it comes to selling something to Mark. The advisor is working in both his own and Mark’s interests – and just so everyone understands, there is nothing illegal about this, in fact, it’s quite common.

But if Mark had an advisor with a FIDUCIARY DUTY on his behalf, that advisor would be required to ONLY act in Mark’s best interests.

A fiduciary is expected to manage the assets FULLY for the benefit of the other person rather than for his or her own profit.

TRUST me, take this detective’s advice – when you are asking for financial advise, also ask whether the advise comes with a FIDUCIARY DUTY,

April is National Financial Literacy Month, Detective Frank Money’s favorite month! Let’s all celebrate by becoming more financially aware!

I’m Frank Money, and I’ve got a question for you. What’s the most expensive purchase you’ll make in your life? A car? Nope. A house? You might think so but you would be wrong. Actually, it’s your retirement. Bet you didn’t even think about that answer.

I’m Frank Money, and I’ve got a question for you. What’s the most expensive purchase you’ll make in your life? A car? Nope. A house? You might think so but you would be wrong. Actually, it’s your retirement. Bet you didn’t even think about that answer.

Here’s the scoop on the case for retirement. Retirement is a long way off. Not even in the horizon – but over the horizon and miles away, and life has more curves than a scenic railroad. Well, there’s some good and there’s some bad with that kind of thinking. Since you do have 30 to 40 years before retirement, investing starting right now will pay off in huge financial dividends down the road.

But you have to do your research with investing, matching 401k’s, having a set amount from your paycheck automatically deposited into your savings and so much more. Matching money from your paycheck from your employer is actually free money – and free money is this gumshoe’s favorite kind of money! As for considering retirement to not even be on the horizon, unless you’re planning to be flipping burgers at 65, this detective strongly suggests you start looking beyond the horizon.

April is National Financial Literacy Month, Detective Frank Money’s favorite month! To celebrate the importance of being financially literate, Detective Money is going to post financial literacy tips every day.

It’s Tax Day!

It’s Tax Day!

Surprise, no it’s not!

This year it’s on Tuesday, April 17th! Thats because of Emancipation Day in Washington D.C. (observed on the weekday closest to April 16), when April 15 falls on a Friday, tax returns are due the following Monday; when April 15 falls on a Saturday or Sunday, tax returns are due the following Tuesday.

If you have filed your taxes and signed on the dotted line, then good for you! If this is your first time, it’s not that far-fetched that you have joined society, contributed to keeping the wheels oiled and turning so our country can keep moving forward. Okay, sometimes I can get carried away.

With your return due next Tuesday, we thought we would share another date with you – Tax Freedom Day – This is the day of the year where everything made up to that date goes to Uncle Sam, and after that date, everything you make is yours. In the United States, it is annually calculated by the Tax Foundation, a Washington, D.C.-based tax research organization. In the U.S., Tax Freedom Day for 2015 was April 24, for a total average effective tax rate of 31 percent of the nation’s income. The latest that Tax Freedom Day has occurred was May 1 in 2000. In 1900, Tax Freedom Day arrived January 22, for an effective average total tax rate of 5.9 percent of the nation’s income.

Tax Freedom Day for 2017 is April 19th! Woo Hoo!

As if you don’t have enough challenges today to secure your finances, there will always be pressure coming from all sides including your friends, co-workers and even the media that will affect the way you spend your money.

Let’s investigate – say you’re still in college and worked all summer to cover some of the cost during the first semester such as, food and your share of the rent and utilities. But on the first night out back at school with your friends, you decided to pick up the tab. It left you short for your first month’s bills and had to dip into your savings that was meant for books.

Or how about that new ultra high-definition TV or subscribing to the NFL Red Zone? And ladies, putting that expensive pair of “must have” shoes on an already maxed-out credit card is not the way to manage your spending effectively.

Best way is to simply walk away from the temptation. Make up a list of financial goals that you can realistically keep. Don’t let outside influences pressure you into forgetting your goals. Your friends will understand.

April is National Financial Literacy Month, Detective Frank Money’s favorite month!

April is National Financial Literacy Month, Detective Frank Money’s favorite month!

To celebrate the importance of being financially literate, Detective Money is going to post financial literacy tips every day.